Tangible exploration assets 1140. Intangible exploration assets

In accordance with current legislative norms, it is necessary to reflect all transactions of a commercial and economic nature in special accounting.

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to know how solve exactly your problem- contact a consultant:

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and FOR FREE!

This also applies to various types of assets – including intangible search assets. This issue is addressed in the legislation in force in the Russian Federation. If possible, you should familiarize yourself with the most significant points in advance.

This way it will be possible to reduce the likelihood of a large number of difficulties and other difficulties associated with the process of conducting audits by tax authorities.

Inappropriately registered intangible assets will lead to fines and other difficulties.

General points

Intangible assets are the property of a company, which is expressed not as tangible property, but as intellectual or some other property.

There are many different types of intangible assets. The regulatory documents reflect their complete list. It is worth familiarizing yourself with all the nuances in advance.

Issues that should be considered in advance include:

- what it is?

- what is their role?

- current standards.

What it is?

Today, on line 1130, intangible search assets must be designated in accordance with legal regulations. But first of all, you should understand the very concept of intangible assets.

Typically, such assets are present in the accounting and tax reporting of an organization that is engaged in the following activities:

- deals with resource discovery;

- carries out development.

This issue is discussed in as much detail as possible in. In this case, the distribution of this type of assets is carried out by the enterprise independently, without outside participation.

Distribution is carried out between the following types of assets:

- intangible search engines;

- for other types of activities.

We should also not forget that the choice made must be reinforced accordingly in the enterprise.

This is necessary to maintain proper accounting and tax records. The issue is covered in detail in. The full list of search-type intangible assets is reflected in the same document.

What is their role

Reflecting assets of this type directly in accounting and tax reporting allows you to implement standard tasks.

These today include the following:

The organization directly receives quite significant benefits from the use of search-type intangible assets. Since they mean information or the right related to the extraction of useful resources.

Moreover, the right to production is often exclusive. There is also depreciation of the type of asset in question.

This question is also worth revealing to yourself in advance. This way you can avoid some difficulties when preparing financial statements.

Current standards

At the moment, there is a fairly large number of various documents directly related to the reflection of intangible exploration assets in reporting.

An equally significant effect is the reflection of their depreciation. The main regulatory document regulating this issue is - it regulates the application.

PBU 14/2007 includes the following:

The process of reflecting information about assets in financial statements must also comply with the regulatory document. The main one is

This legislative act includes the following main sections:

Federal Law No. 402-FZ dated December 6, 2011 includes the following main sections:

| List of objects reflected in the financial statements | |

| Lists the persons who are required to maintain accounting records | |

| How is accounting carried out? | |

| The process of choosing accounting policies and the features of each type are considered. | |

| What are the primary accounting documents? | |

| What are accounting registers | |

| How an inventory of liabilities as well as assets is performed | |

| The procedure for monetary measurement in this type of accounting | |

| What are the requirements for financial reporting? | |

| What is meant by the composition of financial statements | |

| What is the reporting period, as well as the date of reporting | |

| Reporting procedure for | |

| Reporting procedure during the procedure | |

| Internal control | |

| Basic principles related to accounting regulation | |

| A list of documents required in this case is indicated. |

It is important to remember the need to comply with standards regarding the reflection of search-type intangible assets. Since it is often with their help that all sorts of corruption schemes are implemented.

Therefore, the tax service pays the closest possible attention to all this when conducting audits.

In some cases, concealing intangible search assets leads to quite serious disciplinary consequences.

Features of search intangible assets

The intangible search assets themselves have a large number of features and nuances. You should definitely deal with all of them in advance. This will significantly reduce the likelihood of making any mistakes.

Significant issues related to this topic, familiarization with which is strictly necessary, include the following:

- What are intangible search assets?

- How are they reflected in accounting?

- value in tax accounting.

What does this mean?

For 2019, the list of intangible exploration assets includes the following:

| Exclusive or joint right to perform a certain list of works |

|

| Information that was obtained as a result of conducting a certain type of intelligence work |

|

It is important to remember that the actual costs of search assets must include:

- amounts that are paid in accordance with the agreements of the contractor, which is the supplier;

- amounts charged to a specific contractor for performing a volume of work on a special basis;

- a certain commission or other remuneration accrued to the intermediary who provided the opportunity to purchase intangible exploration assets;

- all customs duties without exception, as well as;

- government, patent duties;

- amounts of taxes paid that are not subject to reimbursement;

- depreciation of current as well as non-current assets;

- rewards to employees who directly contribute to the creation of a specific type of asset.

There is also a certain list of actual costs that are not included in the list of those related to the costs of acquiring such assets:

- reimbursement of tax fees;

- general expenses;

- costs that occurred during the process of obtaining a license or are directly related to the process of registering exploration assets.

The points outlined above have the most significant role related to the reflection of information in accounting and tax reporting. It is important to remember that there is no room for error. This can lead to quite serious problems.

How are they reflected in accounting?

It is also worth familiarizing yourself in advance with what kind of account this is – intangible search assets. For these purposes, line No. 1130 is always used.

The reflection process looks like this:

In the case of reflecting depreciation in accounting, the organization must do this starting from the 1st day of the month that follows the month in which the obligation to take into account arose.

Typically the following accounts are used for this:

It is important to remember to consider all different types of search costs. They are recognized as non-current assets. This rule applies to all search assets used.

Before you begin to reflect information in tax and accounting, you should carefully understand all the nuances.

Importance in tax accounting

Assets of this type are taken into account when calculating tax for the use of natural resources. There is a separate section of the Tax Code of the Russian Federation that regulates this issue.

The tax rates are set. A significant factor is the type of mineral. The algorithm for calculating the rate is reflected on the official website of the Federal Tax Service.

There is a fairly large number of different difficulties associated with the process of reflecting intangible search assets.

An important factor is the accounting policy chosen by the enterprise itself. Based on this, the tax base is calculated and other actions are implemented.

Attention!

- Due to frequent changes in legislation, information sometimes becomes outdated faster than we can update it on the website.

- All cases are very individual and depend on many factors. Basic information does not guarantee a solution to your specific problems.

TOPIC 3. BALANCE SHEET OF THE ENTERPRISE

Balance sheet items show the amount of property and liabilities of the enterprise as of a certain date.

Balance sheet item– a separate type of funds (property) or source (liabilities), shown in the balance sheet as a separate item and expressed as a separate amount.

ASSETS

SECTION I. NON-CURRENT CAPITAL includes funds that are heterogeneous in their economic content:

Material resources

Intangible means

Investments, etc.

The combination of these funds in section 1 is due to the long-term nature of their use in the economic activities of the organization and their belonging to the least liquid assets.

Intangible assets (line 1110)– indicates the amount of the residual value of the intangible assets at the end of the reporting period.

The residual value of intangible assets, depending on the procedure for accounting for depreciation of intangible assets adopted in the accounting policy:

or immediately formed on account 04 “Intangible assets”;

or calculated by subtracting from the balance at the end of the year in account 04 the balance at the end of the year in account 05 “Amortization of intangible assets”.

In accordance with clause 3 of PBU 14/2007 “Accounting for intangible assets”, an object is accepted in accounting as an intangible asset if the following conditions are simultaneously met:

1. the object is capable of bringing economic benefits to the organization in the future, in particular, the object is intended:

For use in production of products;

When performing work or providing services;

For the management needs of the organization.

2. there is a right to receive economic benefits that this object is capable of bringing in the future, including the organization has properly executed documents confirming the existence of the asset itself and the right of this organization to the result of intellectual activity or a means of individualization:

Patents;

Evidence;

Other security documents;

Agreement on the alienation of the exclusive right to the result of intellectual activity or to a means of individualization;

Documents confirming the transfer of exclusive rights without a contract;

There must also be restrictions on the access of other persons to such economic benefits (control over the object).

3. the possibility of separating or separating (identifying) an object from other assets;

4. The object is intended to be used for a long time, i.e. useful life exceeding 12 months;

5. the organization does not intend to sell the property within 12 months;

6. the actual (initial) cost of the object can be reliably determined;

7. the object does not have a material form.

In accordance with Article 1225 of Chapter 69 of the Civil Code, the results of intellectual activity and equivalent means of individualization of legal entities, goods, works, services and enterprises that are granted legal protection (intellectual property) are:

Works of science, literature and art; programs for electronic computers (computer programs); Database; phonograms; communication on the air or via cable of radio or television programs (broadcasting by broadcasting or cable broadcasting organizations); inventions; breeding achievements; brand names; trademarks and service marks.

Also, licenses for the use of software products (such as 1c programs, antiviruses, etc.) do not apply to intangible assets.

In accordance with paragraph 16 of PBU 14/2007, the initial/actual cost of intangible assets at which it is accepted for accounting is not subject to change, except in cases of revaluation and depreciation of intangible assets.

An organization can revaluate intangible assets at the end of the reporting period. The use or waiver of this right must be formalized in the accounting policy for accounting purposes. Revaluation of intangible assets is carried out by recalculating their residual value (clause 19 of PBU 14/2007).

The amount of additional valuation of intangible assets as a result of revaluation is credited to the additional capital of the organization. The subsequent amount of markdown within the revaluation limits reduces the additional capital. The amount of the markdown is included in the financial result as other expenses. Subsequent revaluation within the limits of the previous depreciation amount - to the financial result as part of other income.

By line 1110 the residual value of intangible assets is reflected: = debit balance in account 04 “Intangible assets” (excluding R&D expenses) minus credit balance on account 05 “Amortization of intangible assets”

If depreciation is calculated without using account 05, then this line reflects: Debit balance of account 04 “Intangible assets” (excluding R&D expenses)

Research and development results (line 1120). This line indicates the amount of expenses for completed research, development and technological work (hereinafter referred to as R&D*), not written off as expenses for ordinary activities and other expenses. *Research work includes work related to the implementation of scientific (research), scientific and technical activities and experimental developments, defined by the Federal Law of August 23, 1996. No. 127-FZ “On science and state scientific and technical policy.”

In accordance with clause 16 of PBU 17/02 “Accounting for expenses on research, development and technological work”, if significant, information on R&D expenses is reflected in the balance sheet for a separate group of asset items (section “Non-current assets”) .

The organization's expenses on R&D, the results of which are used for the production or management needs of the organization, are accounted for on account 04 “Intangible assets” separately in accordance with the Chart of Accounts and the Instructions for its application.

In accordance with clause 2 of PBU 17/02, the following are taken into account as part of R&D:

R&D for which results were obtained that are subject to legal protection, but were not formalized in the manner prescribed by law;

R&D that produced results that are not subject to legal protection in accordance with the norms of current legislation.

As part of R&D, account 04 is not taken into account and is not reflected on line 1120:

Unfinished R&D, as well as R&D, the results of which are taken into account in accounting as intangible assets; expenses of the organization for the development of natural resources (conducting geological studies of subsoil, exploration (additional exploration) of developed deposits;

Preparatory work in extractive industries, etc.;

Costs for preparation and development of production, new organizations, workshops, units (start-up costs);

Costs of preparing and mastering the production of products not intended for serial and mass production;

Costs associated with improving technology and production organization, improving product quality, changing product design and other operational properties carried out during the production (technological) process.

In accordance with clause 9 of PBU 17/02, R&D expenses include all actual expenses associated with the implementation of the specified work.

Expenses for R&D include:

Cost of materials and equipment and services of third-party organizations and persons used in performing the specified work;

Costs of wages and other payments to employees directly involved in performing the specified work under an employment contract;

Contributions for social needs;

Cost of special equipment and special fittings intended for use as test and research objects;

Depreciation of fixed assets and intangible assets used in performing the specified work;

Costs for the maintenance and operation of research equipment, installations and structures, other fixed assets and other property;

General business expenses, if they are directly related to the implementation of these works;

Other expenses directly related to the implementation of research, development and technological work, including testing costs.

By line 1120 information on expenses for completed research, development and technological work (R&D) is reflected: = debit balance in account 04 “Intangible assets” (analytical account for accounting for R&D expenses)

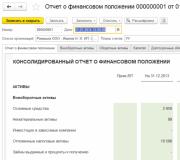

Line 1130 “Intangible exploration assets”

By line 1130 the costs of searching, assessing mineral deposits and exploring mineral resources in a certain subsoil area are reflected: =

debit balance on account 08 “Investments in non-current assets” (analytical account for accounting of legal entities) minus

Withcredit balance for account 05 “Amortization of intangible assets” (analytical accounts for accounting for depreciation and impairment of legal acts)

Intangible search assets may be reflected in the accounting of organizations that carry out costs for searching, evaluating mineral deposits and exploring mineral resources in a certain subsoil area (clause 2 of PBU 24/2011).

Organizations independently distribute search costs between non-current assets (including intangible search assets) and expenses for ordinary activities (clause 4 of PBU 24/2011). The choice made by the organization is fixed in the accounting policy for accounting purposes (clause 7 of PBU 1/2008).

What are intangible search assets?

a) the right to carry out work on the search, assessment of mineral deposits and (or) exploration of mineral resources, confirmed by the presence of an appropriate license;

b) information obtained as a result of topographical, geological and geophysical studies;

c) results of exploratory drilling;

d) results of sampling;

e) other geological information about the subsoil;

f) assessment of the commercial feasibility of production (clause 8 of PBU 24/2011).

Intangible search assets: details for the accountant

- The procedure for filling out the balance sheet in a general form. Example

For R&D). Line 1130 “Intangible exploration assets” = Dt 08 (analytical account...

- Accounting for intellectual property

The list of costs included in the cost of intangible search assets based on the recommended standard, the organization... the actual costs of acquiring (creating) intangible search assets can, for example, be included: - the cost of a license... the accounting unit for tangible and intangible search assets is determined by the organization in relation to the rules... 10 months) - depreciation of an intangible exploration asset was accrued for the period March - December...

- Reclassification of tangible search assets into intangible assets

Tangible and as part of intangible search assets. In accordance with paragraph... are transferred to fixed assets, intangible search assets - to the intangible assets of the organization... requalification of search assets - transfer of an intangible search asset into a tangible asset. In this...hereinafter - ILA) or as part of intangible search assets (hereinafter - ILA). One of... the costs of acquiring (creating) intangible exploration assets includes the costs of drilling support...

- What to consider when preparing financial statements for 2013

The balance of account 08 is the subaccount “Intangible exploration assets” and from it subtract... the subaccount “Amortization and impairment of intangible exploration assets.” A similar situation with the line...

- Changes in legislation for accountants from 01/26/2012

They are classified as tangible and intangible, respectively. Search assets are valued based on the amount of actual costs... a procedure has been established for assessing tangible and intangible search assets. Minimum indicators of impairment identified, analysis...

- 12 recommendations to help you pass an audit

... “Tangible exploration assets” and (or) “Intangible exploration assets” (clause 6 of PBU 24/2011 ...). Recommendation 11. In the balance sheet, the indicators “Intangible exploration assets” and “Tangible exploration assets” can be...

- What should you pay special attention to when preparing financial statements for 2012?

Balance sheet as tangible or intangible search assets in the section “Non-current assets”. This...

- Practice of the Supreme Court of the Russian Federation on tax disputes for June 2017

The taxpayer confirmed the commercial feasibility of the acquired intangible exploration assets (geological information, characterization report...

- Purpose of the article: display of material costs associated with the search, analysis and exploration of deposits, analysis of minerals.

- Line number in the balance sheet: 1140.

- Account number according to the chart of accounts: debit balance of the subaccount .12 minus the credit balance of the account. (in terms of depreciation and impairment of these objects).

Tangible exploration assets mean non-current assets on the balance sheet of an organization that have a tangible form. The main characteristic of this type of object is the purpose of use. According to the current legislation, the costs incurred when using assets in the process of searching for, analyzing mineral deposits, as well as exploration of minerals in a certain subsoil area are regulated.

Note from the author! This type of costs includes non-current assets used by the enterprise in subsoil areas until there is official documentary evidence of the commercial feasibility of extracting minerals in a given deposit, subject to the technical equipment and availability of resources of the enterprise. Recognition of exploration expenses as non-current assets of the company is carried out, as a rule, if there is a license in a certain subsoil area where exploration activities are carried out.

Material exploration assets are the company’s expended material resources associated with the acquisition or formation of objects with a tangible form, namely:

- systems of structures (for example, gas pipelines, etc.);

- specialized equipment (drill, pumps, etc.);

- units of transport.

Acceptance of costs in company accounting

The company independently decides on the types of costs included in non-current assets. All other costs are written off in accounting as expenses for ordinary activities.

In accounting, tangible search assets are taken in the amount of all actual costs incurred for their creation and use in the company’s activities.

Composition of actually incurred costs included in the cost of a non-current exploration asset:

- cost of goods and services of suppliers according to the contract;

- the cost of work performed under construction contracts and other agreements;

- payment of a bonus to intermediary counterparties through whom the search asset was purchased;

- payment for information and consulting services;

- payment of mandatory customs duties;

- taxes and duties, the further reimbursement of which is not possible;

- the amount of accrued depreciation of other non-current assets of the company used in the formation of a new exploration asset;

- remuneration of employees involved in the process of creating an asset;

- fulfilled obligations of the company in relation to environmental protection, liquidation of buildings and structures related to the implementation of prospecting and exploration activities in the subsoil, as well as mineral exploration;

- other costs incurred in creating or purchasing a search asset.

Note from the author! If an enterprise plans to use these non-current assets in activities after completion of exploration activities at a certain subsoil site, the assets can be transferred and included in the company’s fixed assets (Dt01 Kt08.12).

Line 1140 of the balance sheet contains information about the actual costs of creating assets, taking into account adjustments for revaluation and the amount of depreciation as of December 31 of the reporting year, the previous one and the previous one.

Impairment risk assessment

According to PBU, the company is required to monitor at each reporting date in order to identify possible signs of impairment of exploration assets. The following factors should be analyzed:

- validity period of the license for prospecting, evaluation of deposits and exploration of mineral resources (expiration within a year after the reporting period in the absence of plans to issue an extension of license permits);

- discrepancy between planned costs and actual expenditures of funds for the implementation of activities for the search and analysis of deposits, as well as resource exploration;

- making a final decision by the company to terminate prospecting and exploration work in this area;

- The monitoring carried out indicates the impossibility of paying off the costs of searching and evaluating deposits in full.

Case Study

A joint-stock company engaged in the search and development of oil fields attracted Solnyshko LLC to drill a well. The cost of the work amounted to 5 million rubles, including VAT of 762.7 thousand rubles. The data analysis revealed that oil production in this area was inappropriate, and the well was abandoned.

Business transactions in the accounting of JSC:

- Dt08 Kt60

4.2 million rubles - the cost of the contractor’s work excluding VAT.

- Dt19 Kt60

762.7 thousand rubles. - VAT included.

- Dt68 Kt19

762.7 thousand rub. - acceptance of VAT for deduction.

- Dt91.2 Kt08

4.2 million rubles. - write-off of a exploration asset due to the inexpediency of further oil production activities.

Normative base

Data on the material resources expended during the search and analysis of deposits must be reflected in accordance with PBU 24/2011, approved by order of the Ministry of Finance of the Russian Federation dated October 6, 2011 No. 125n.

Common entries for accounting for tangible exploration assets

- Formation of the initial accounting price of a material exploration asset in accounting.

Dt08.12 Kt60 - payment to suppliers.

Dt08.12 Kt70 - remuneration of employees involved in the creation process.

Dt08.12 Kt10 - materials used.

Note! Postings with accounts 69,02,96, etc. can also be generated.

- Impairment of a tangible exploration asset.

Dt91.02 Kt08.12 - recognition of loss.

Dt02 Kt91.1 - adjustment of accrued depreciation.

- Transfer of existing material search facilities to the main equipment section.

Dt01 Kt08.12.

- Write-off of incurred costs due to the futility of their further use in the company's activities (for example, due to damage).

A selection of the most important documents upon request Material prospecting assets(regulatory legal acts, forms, articles, expert consultations and much more).

Regulatory acts: Material prospecting assets

6. Exploration costs related primarily to the acquisition (creation) of an object that has a tangible form are recognized as tangible exploration assets. Other search assets are recognized as intangible search assets.

Order of Rosstat dated November 22, 2017 N 772

(as amended on December 29, 2018)

"On approval of the Instructions for filling out federal statistical observation forms N P-1 "Information on the production and shipment of goods and services", N P-2 "Information on investments in non-financial assets", N P-3 "Information on the financial condition of the organization", N P-4 "Information on the number and wages of employees", N P-5 (m) "Basic information about the activities of the organization" Line 39 reflects fixed assets, both in operation and those under reconstruction, modernization, restoration, conservation or reserve, in lease, in trust management, at residual value (with the exception of fixed assets for which, in accordance with the established procedure no depreciation is charged). On this line, organizations making profitable investments in material assets provided for a fee for temporary possession and use (including under a financial lease agreement, under a rental agreement), in order to generate income, reflect the residual value of the specified property. Line 39 reflects tangible exploration assets that are recognized as non-current assets. To fill in line 39, account data 01, 02, 03, 08 is used.